The Definitive Guide for Chapter 13 Bankruptcy Lawyers In Md

Bankruptcy doesn't mean that you get stripped to your shorts and thrown out on the street. Far from it. In fact, there are several different types of bankruptcy, all with their own procedures and rules, that are designed to accomplish different goals. Federal law provides for five types of bankruptcy.

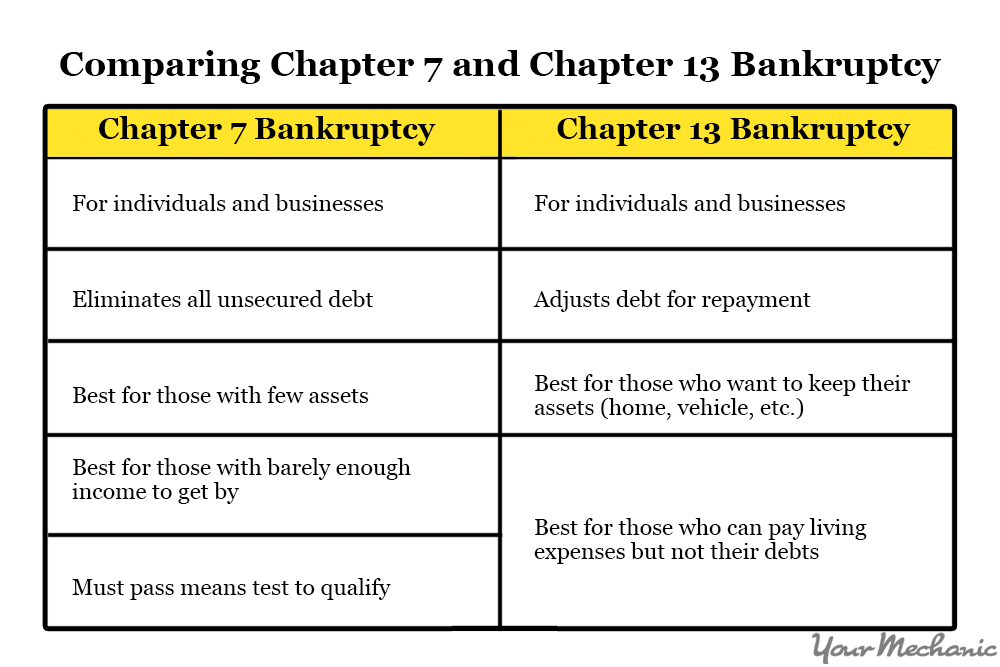

Of these, most people file under Chapter 7,* a process that allows for forgiveness of debt (also called discharge of debt) in exchange for the filer's nonexempt assets (assets that are deemed under state or federal law to be nonessential to a fresh start,) The second most common type of bankruptcy for individuals is a Chapter 13* case.

The Chapter 13 process requires that the debtor (that’s what we call the person who files the bankruptcy case) make a monthly payment to a Chapter 13 Trustee for a period of 36 to 60 months. The Trustee then distributes that money to the debtor’s creditors who have filed proper claims..

The Best Strategy To Use For Cheap Chapter 13 Bankruptcy Lawyers Md

The Code is divided into numbered chapters and sections. Hence we refer to each type of bankruptcy by the number of the Bankruptcy Code chapter that covers it. Discharge of debt in exchange for nonexempt (nonessential) property. Reorganization of debt, usually more effective for high debt/high asset individuals and business interests Reorganization reserved for family farmers, small farming concerns, and fishermen, that draws elements from Chapter 11 and Chapter 13 A monthly payment plan for managing debt that lasts three to five years and usually results in a discharge.

The difference is in how a debtor gets to the discharge. In a Chapter 7 case, he is required to turn over any nonexempt property. Exempt property is defined under federal or state law and is usually property deemed necessary for the debtor to achieve a fresh start after the bankruptcy is over.

In a Chapter 13 case, instead of turning over property for a trustee to sell, the debtor makes payments for 36 to 60 months to a Chapter 13 trustee who distributes the funds to creditors who have filed claims that the court agrees are proper. So, why would someone file a Chapter 13 case that can last as long as five years when a Chapter 7 case usually lasts about six (6) months? There are a number of factors that go into that decision - chapter 13 bankruptcy lawyers baltimore MD.

Not known Details About Cheap Chapter 13 Bankruptcy Lawyers Md

A word about the Means Test The Means Test is a calculation applied to almost every consumer Chapter 7 bankruptcy case and is purportedly designed to determine whether the debtor has enough disposable income to fund a meaningful Chapter 13 plan. If so, the debtor is said to be filing the Chapter 7 case under a "presumption of abuse," that is, the bankruptcy laws would rather have that debtor making payments for a period of time and paying back at least a portion of debt, rather than get an outright discharge of the debt.

There are many reasons why a debtor would choose to file a Chapter 13 despite the Means Test. Chapter 13 may provide a debtor with bankruptcy protection even if he makes too much money to qualify for a Chapter 7 case or if he received a discharge in a prior Chapter 7 case.Chapter 13 allows a debtor the length of the plan to pay back past due amounts owed on houses, cars and other loans that have collateral.Chapter 13 allows a debtor to pay past due income taxes and domestic support obligations like child support and alimony over the three to five year Chapter 13 payment plan.Chapter 13 may allow a debtor to set new terms for the payment of a car loan that is older than 2.5 years.Chapter 13 protects the debtor's co-signer on a personal loan from having to pay.Chapter 13 may allow the debtor to better manage high student loan payments.Chapter 13 allows the debtor to protect property that he might have to give up in a Chapter 7 case.Chapter 13 may allow the debtor to pay his bankruptcy attorney’s fee as a part of the Chapter 13 plan payment instead of all up front.

The payments last from 36 to 60 months and may include an amount that will go to unsecured creditors, past due taxes, child support, and past due home mortgage amounts. It may even include car or house payments and some portion of a debtor's attorneys fees. It is designed to Help make payment of unsecured debts like medical bills and credit cards more affordable and manageable.Provide a way to pay past due house, car, income tax, child support and alimony payments over time.Substitute for the need to sell or turn over nonexempt property.

The Chapter 13 Bankruptcy Lawyers In Md Statements

When debts become overwhelming, many people seek one of two types of bankruptcy for relief, depending on their income and needs. For instance, people with little income remaining at the end of each month and minimal assets usually choose to file for Chapter 7 bankruptcy, the chapter that wipes out (discharges) qualifying debt in four to six months without the need to repay creditors.

In exchange for debt relief, these filers pay their discretionary income to their creditors over the course of a three- to five-year repayment plan. In this article, you’ll learn about how the overall Chapter 13 process works. Chapter 13 bankruptcy isn't for everyone. Maryland chapter 13 bankruptcy lawyers. Here are a few requirements you should know upfront.

(Find the figures in What Are Chapter 13 Bankruptcy Debt Limitations?) A "secured debt" gives a creditor the right to take property (such as your house or car) if you don't pay the debt. An "unsecured debt" (such as a credit card or medical bill) doesn't give the creditor this right.

What Does Maryland Chapter 13 Bankruptcy Lawyers Do?

When you file a Chapter 13 case, you’ll have to prove to the court that you can afford to meet both your monthly household obligations and pay into a repayment plan. If your income is irregular or too low, the court won’t confirm (approve) your proposed repayment plan (more below) (cheap chapter 13 bankruptcy lawyers MD).

student loan insolvency coal company bankruptcy free bankruptcy attorney advice